Buying shares is easy. Owning them calmly through earnings surprises, recessions, interest-rate changes, and market panic is much harder.

That is why better risk control matters. If you want to invest in shares successfully over time, the goal is not to avoid every loss. Losses are part of investing. The goal is to make sure no single decision, stock, sector, or emotion can do serious damage to your financial future.

This guide explains a practical way to invest shares with better risk control, from setting a risk budget before you buy to sizing positions, diversifying, reviewing businesses, and building rules you can follow when markets become uncomfortable.

This article is educational, not personal financial advice. Your best decisions depend on your goals, time horizon, income, tax situation, and risk tolerance.

What Better Risk Control Really Means

Many new investors think risk control means finding stocks that will not fall. That is impossible. Even excellent companies can decline sharply when expectations change, valuations compress, or the whole market sells off.

Better risk control means building an investment process that can survive mistakes. It means accepting uncertainty while limiting the size and consequences of being wrong.

For share investors, the main risks usually include:

| Risk type | What it means | How to control it |

|---|---|---|

| Business risk | The company performs worse than expected | Study earnings, cash flow, debt, competition, and management quality |

| Valuation risk | You pay too much for a good business | Compare price to earnings, cash flow, growth, and industry peers |

| Concentration risk | Too much money depends on one stock or sector | Use position limits and diversify across companies and industries |

| Liquidity risk | You cannot buy or sell at a reasonable price | Prefer liquid shares and use limit orders when appropriate |

| Behavioral risk | Fear, greed, or overconfidence drives decisions | Use written rules, checklists, and planned review dates |

| Time-horizon risk | You need the money before the investment has time to recover | Keep short-term money outside volatile shares |

Notice that most of these risks are controllable before you buy. That is the key point. Good investors do not wait until prices fall to think about risk. They design risk control into the portfolio from the beginning.

Start With a Risk Budget, Not a Stock Tip

Before asking, “Which share should I buy?” ask, “How much risk can I afford to take?”

A risk budget is a simple set of limits that tells you how much of your capital can be exposed to shares, how much can go into any single company, and how much loss would force you to rethink your plan.

Your risk budget should reflect three things: your time horizon, your financial stability, and your emotional tolerance. A long-term investor with stable income and an emergency fund can usually tolerate more volatility than someone who may need the money in two years.

| Time horizon for the money | Main priority | Risk-control focus |

|---|---|---|

| Under 3 years | Capital preservation | Avoid relying heavily on shares for money needed soon |

| 3 to 7 years | Balance | Use diversification and moderate position sizes |

| 7 years or more | Long-term growth | Accept volatility, but control concentration and valuation risk |

If you are new, keep the first version of your risk budget simple. For example, decide your maximum allocation to shares, your maximum allocation to any one stock, and your maximum allocation to one sector. These limits prevent excitement from turning into overexposure.

For a broader foundation, Greek Shares also explains portfolio-level thinking in How to Manage Portfolio Risk Wisely.

Diversify Before You Try to Be Clever

Diversification is one of the most practical risk-control tools available to individual investors. It does not guarantee profits or prevent losses, but it reduces the chance that one bad company-specific event ruins your portfolio.

A diversified share portfolio should not simply contain many stocks. Ten banks are not true diversification if they all depend on the same interest-rate environment and credit cycle. Good diversification spreads exposure across different industries, business models, regions, and return drivers.

For many beginners, broad funds or ETFs can provide a diversified core before adding individual shares. This is why the choice between funds and individual stocks matters. If you are unsure where to begin, review the Greek Shares guide on Index Funds vs Stocks to understand the trade-offs.

A useful structure is the core-and-satellite approach. The core of the portfolio is diversified and relatively simple, often built with broad funds. The satellite portion is smaller and may include individual stocks you have researched carefully. This lets you learn stock selection without making your entire financial future depend on a few picks.

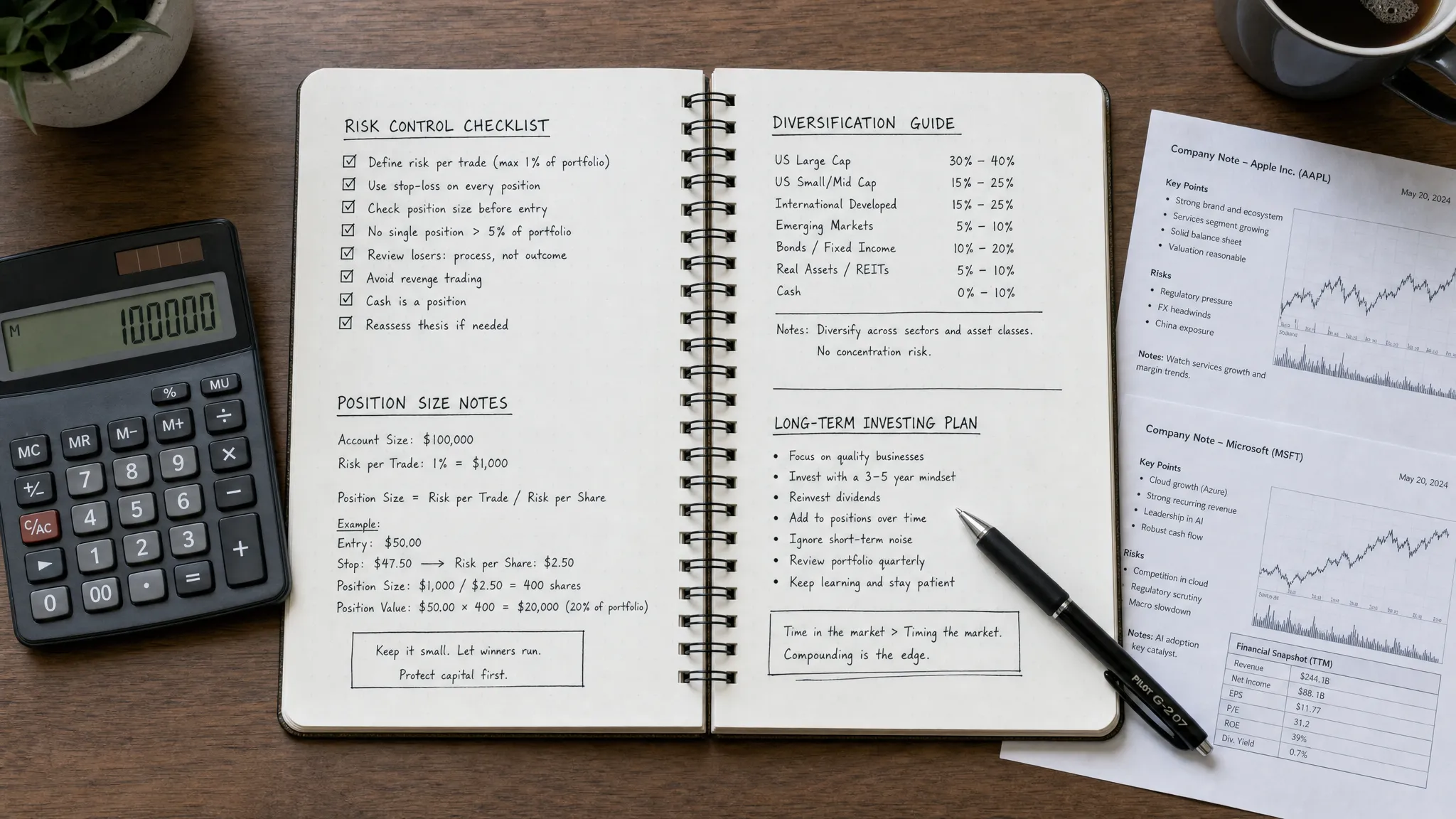

Use Position Sizing to Limit Damage

Position sizing is the discipline of deciding how much money to put into each investment. It is one of the clearest ways to control risk because it converts uncertainty into a measurable decision.

Imagine a $10,000 portfolio. If you put $5,000 into one stock and it falls 50%, your portfolio loses 25%. If you put $500 into that same stock and it falls 50%, your portfolio loses 2.5%. The stock’s decline is the same, but the portfolio damage is completely different.

That is why position size often matters more than being right or wrong on one idea.

Here is a simple way to think about it:

| Position size | If the stock falls 40% | Portfolio impact |

|---|---|---|

| 2% of portfolio | Loss of 0.8% of portfolio | Usually manageable |

| 5% of portfolio | Loss of 2% of portfolio | Noticeable but controlled |

| 10% of portfolio | Loss of 4% of portfolio | Significant |

| 25% of portfolio | Loss of 10% of portfolio | Potentially damaging |

These are not universal recommendations. They are examples showing how position size changes portfolio risk. Your own limits should depend on your experience, diversification, and ability to tolerate losses.

Also be careful with averaging down. Buying more after a decline can make sense if the business value is intact and the valuation is more attractive. It is dangerous if you are only trying to avoid admitting a mistake. Set a maximum position size in advance so that “buying the dip” does not become uncontrolled concentration.

Research the Business, Not Just the Price Chart

A share is not just a ticker symbol. It represents ownership in a business. Better risk control starts with understanding what you own and why you own it.

Before buying an individual stock, study the company’s business model, competitive position, financial statements, debt, profit margins, cash flow, and valuation. You do not need to predict the future perfectly. You do need a reasonable explanation of how the business makes money, what could go wrong, and what price would make the risk attractive.

A basic stock-research checklist should include:

- What does the company sell, and who are its customers?

- Are revenue and earnings growing consistently or cyclically?

- Does the company generate free cash flow?

- How much debt does it carry, and can it service that debt?

- Does management allocate capital wisely?

- Is the valuation reasonable compared with earnings, cash flow, assets, and growth?

- What would prove your investment thesis wrong?

If this process feels unfamiliar, start with How to Analyze a Company Stock. You can also strengthen your valuation discipline by studying the P/E Ratio Explained for Stock Investors and learning How to Read Earnings Reports Clearly.

The important point is not to make analysis complicated. The important point is to avoid buying shares only because they are popular, cheap-looking, or rising fast.

Control Your Entry Price and Buying Method

Even a good company can be a poor investment if bought at an excessive price. Better risk control includes how you enter a position.

There are three common ways to reduce entry risk.

First, use valuation discipline. Decide what you believe the business is worth, then compare that estimate to the market price. You do not need false precision, but you should know whether you are paying a sensible price or relying on optimism.

Second, consider staged buying. Instead of investing the full amount at once, you can build the position gradually. This reduces the emotional pressure of choosing the perfect day to buy. Greek Shares explains this concept in What Is Dollar Cost Averaging?.

Third, understand order types. A market order prioritizes execution, while a limit order prioritizes price. For liquid, widely traded shares, market orders may work well during normal market hours. For less liquid shares or volatile conditions, a limit order can help avoid paying much more than intended. See Limit Order vs Market Order Explained for a practical comparison.

Buying discipline matters because investors often take too much risk at the moment of maximum excitement. A planned buying method slows the process down and reduces impulsive decisions.

Decide When You Will Sell Before You Need To

Many investors spend hours deciding what to buy and almost no time deciding when they would sell. That is a mistake.

A sell plan protects you from two opposite errors: panic selling after normal volatility and refusing to sell when the investment case has clearly deteriorated.

Good sell rules are usually connected to the original thesis. For example, you might consider selling if the company’s competitive advantage weakens, debt becomes dangerous, management credibility declines, or the stock becomes so overvalued that future returns no longer justify the risk.

You may also sell for portfolio reasons. If one position grows too large, trimming it can reduce concentration risk even if you still like the company. If your life goals change, your portfolio may need to become more conservative.

Stop-loss orders and trailing stops can be useful for some traders, but they are not perfect. In volatile markets, a stop can trigger during a temporary decline and remove you from a strong long-term investment. Long-term investors often benefit more from review rules than automatic selling rules.

A practical approach is to write down three things before buying: why you are buying, what would make you wrong, and when you will review the position. For a deeper discussion, read When to Sell Stocks and When to Hold.

Avoid Leverage Until You Fully Understand the Consequences

Borrowed money magnifies both gains and losses. Margin can make a small decline financially and emotionally larger than expected. It can also force you to sell at the worst possible time through margin calls.

For most beginners, avoiding leverage is one of the simplest forms of risk control. If you cannot comfortably own a position without borrowed money, the position is probably too large.

The same caution applies to complex instruments such as options, CFDs, futures, and highly leveraged products. These tools can have legitimate uses, but they require knowledge, discipline, and risk limits. Complexity is not the same as sophistication. Often, the more complex the product, the more important it is to understand the downside before thinking about potential returns.

Build a Review System, Not a Prediction System

Better risk control does not require predicting every market move. It requires a review system that keeps your portfolio aligned with reality.

A review system should answer basic questions at regular intervals. Are your holdings still consistent with your goals? Has one stock become too large? Has a business deteriorated? Are you reacting to headlines or following your plan? Have market gains made you more aggressive than you intended?

This kind of discipline is similar to good learning. People improve when they receive feedback, reflect on mistakes, and take more responsibility over time. Even outside finance, adaptive learning environments are built around the idea that challenge, feedback, and growing autonomy help people develop better judgment. Investors can use the same principle: learn from decisions, review outcomes, and gradually improve the process.

An investing journal can make this practical. Record the date, stock, purchase reason, valuation view, risks, position size, and planned review trigger. Later, compare what happened with what you expected. Over time, your journal will reveal patterns: whether you chase performance, sell too early, ignore debt, overpay for growth, or become too confident after a few winners.

Greek Shares also covers the behavioral side of investing in Investor Psychology for Beginners Explained, which is highly relevant to risk control.

A Simple Risk-Control Checklist Before Buying Shares

Use this checklist before making a new investment. It is designed to slow you down and make hidden risks visible.

| Question | Strong answer | Warning sign |

|---|---|---|

| Do I understand the business? | You can explain how it makes money in plain language | You only know the ticker or story |

| Why is this stock attractive now? | Valuation, business quality, and expected return are reasonable | You are buying because it has gone up |

| How large will the position be? | It fits your pre-set limit | You are making an exception because you feel confident |

| What could go wrong? | You can name business, valuation, and market risks | You believe the stock is “safe” because it is popular |

| What would make me sell? | You have thesis-based sell rules | You plan to decide later under pressure |

| How does it affect diversification? | It improves or maintains balance | It adds more exposure to a sector you already own |

| Is this money needed soon? | No, it fits your time horizon | Yes, but you hope the stock rises quickly |

If you cannot answer these questions, you do not necessarily need to abandon the idea. You may simply need more research, a smaller position, or a diversified fund instead of an individual stock.

Common Risk-Control Mistakes to Avoid

Risk control often fails because of simple, repeated mistakes rather than one dramatic decision.

One common mistake is confusing a low share price with low risk. A stock trading at $2 is not automatically safer than a stock trading at $200. Risk depends on business quality, valuation, balance sheet strength, liquidity, and future expectations.

Another mistake is overconfidence after early success. A few winning trades can make investors increase position sizes too quickly. Markets often punish confidence that has not yet been tested by a full cycle.

A third mistake is ignoring correlation. You may think you own different companies, but if they all depend on the same commodity price, interest-rate trend, consumer cycle, or technology theme, they may fall together.

A fourth mistake is investing money that should remain in cash. Emergency funds, near-term tuition, home deposits, or essential expenses should not depend on short-term market performance.

Finally, many investors confuse activity with control. Trading more often does not automatically reduce risk. Sometimes the best risk-control decision is to do nothing because your original plan remains valid.

Frequently Asked Questions

Is investing in shares too risky for beginners? Investing in shares carries risk, but beginners can reduce avoidable risk by starting small, using diversified funds, learning basic analysis, avoiding leverage, and keeping short-term money outside the stock market.

How many shares should I own for diversification? There is no perfect number. A few individual stocks may leave you exposed to company-specific risk, while too many may become difficult to understand and monitor. Many beginners use diversified funds as a core holding and add individual shares gradually.

Should I use stop-loss orders for risk control? Stop-loss orders can help some traders limit losses, but they can also trigger during temporary volatility. Long-term investors may prefer position sizing, diversification, and thesis-based review rules instead of automatic exits.

What is the biggest risk when investing in shares? The biggest risk is often not volatility itself, but permanent loss of capital caused by overpaying, owning weak businesses, concentrating too much, using leverage, or making emotional decisions during market stress.

Can I invest in shares without trying to time the market? Yes. Many investors use regular contributions, staged buying, diversification, and long-term holding periods instead of trying to predict short-term market movements.

Build Risk Control Before Your Next Purchase

If you want to invest shares with better risk control, do not begin with predictions. Begin with structure.

Set a risk budget. Diversify intelligently. Keep position sizes reasonable. Study the business. Control your entry price. Write down your sell rules. Review your decisions. Most importantly, build a process you can follow when markets are exciting and when they are frightening.

Risk can never be eliminated, but it can be managed. Greek Shares offers investing guides, tutorials, and educational articles to help you keep improving your process. Continue with How to Buy Your First Stock the Right Way or explore the Beginner Portfolio Building Guide to strengthen your foundation before your next investment decision.

{kind=link}