No single asset, sector, or strategy performs best in every stock market cycle. The winner changes because the forces that drive returns change: earnings growth, interest rates, inflation, credit conditions, investor sentiment, and valuations.

A simple way to think about it is this: early in a recovery, investors often reward companies whose profits can rebound sharply. Late in a cycle, they often prefer companies that can defend margins and cash flows. During recessions, the best performer may not be a stock at all, but cash, high-quality bonds, or defensive equity sectors.

The goal is not to predict the next turn perfectly. It is to understand which areas of the market tend to lead, which tend to lag, and how to build a portfolio that can survive the full cycle. This article is educational and not personal financial advice.

The short answer: leadership rotates

If you are asking what performs best in stock market cycles, the honest answer is: it depends on the phase of the cycle and the price you pay.

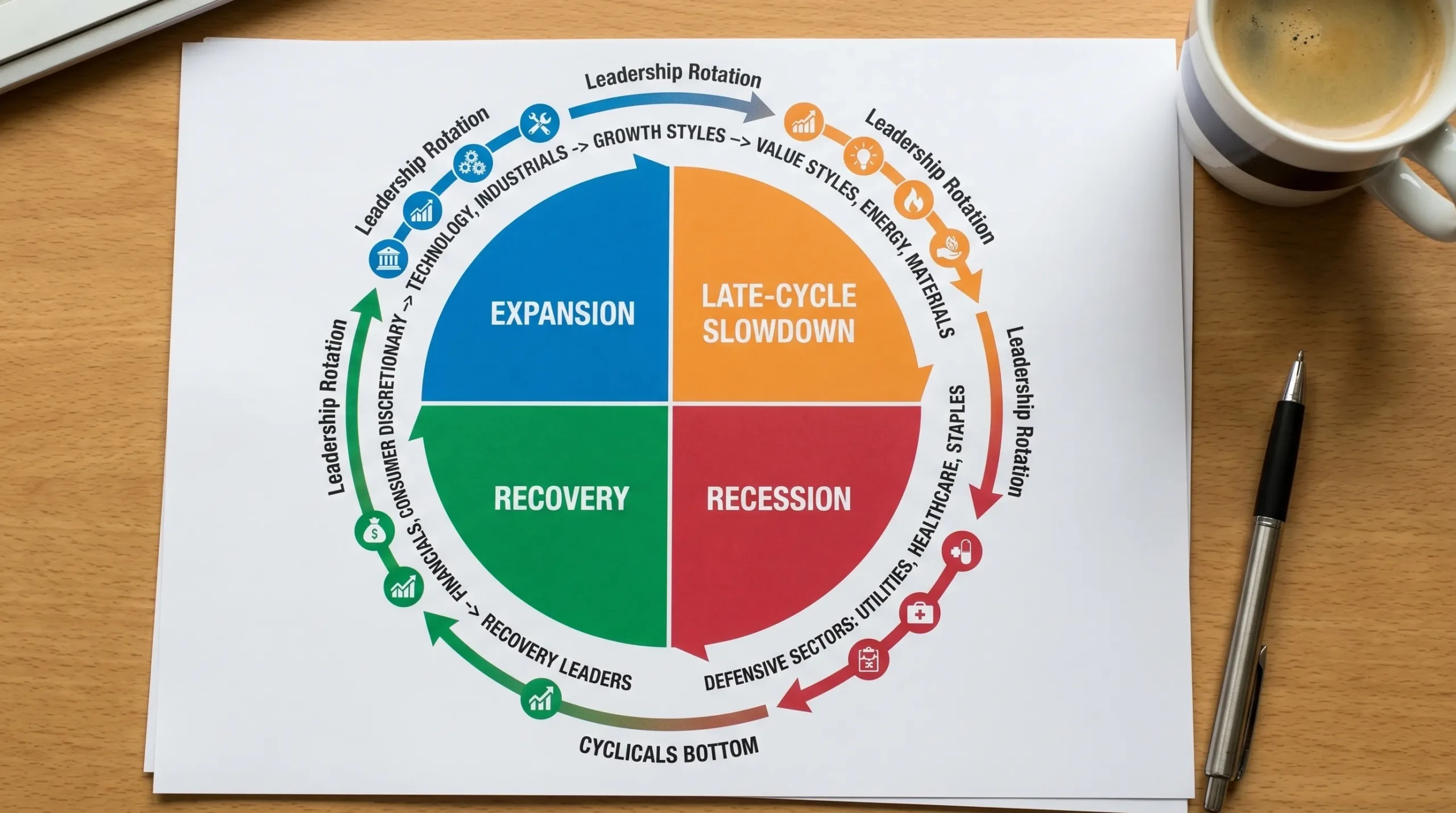

The table below gives a practical overview.

| Cycle phase | Typical backdrop | Areas that often perform well | Areas that often struggle |

|---|---|---|---|

| Early recovery | Growth improves from a weak base, rates may be falling, earnings expectations are low | Cyclical stocks, small caps, financials, consumer discretionary, industrials, broad equity indexes | Cash, overly defensive positioning, companies that cannot recover earnings |

| Mid-cycle expansion | Growth is steady, profits improve, inflation is usually manageable | Quality growth, technology, healthcare, industrials, diversified equity exposure | Highly speculative stocks with no earnings, overvalued themes |

| Late cycle | Growth slows, inflation and rates may be elevated, margins come under pressure | Energy, materials, value stocks, dividend growers, consumer staples, healthcare, utilities, short-duration bonds | Long-duration growth stocks, highly leveraged companies, low-quality cyclicals |

| Recession or bear market | Earnings fall, credit tightens, unemployment rises, fear increases | Cash, short-term government bills, high-quality bonds, defensive sectors, strong balance sheets | High-beta stocks, weak balance sheets, overleveraged businesses |

| New bull market | Sentiment is still cautious, but markets begin discounting better conditions | Broad equities, cyclicals, small caps, quality companies bought at lower valuations | Investors who remain fully out of the market too long |

These are tendencies, not laws. A strong company in a weak sector can still outperform. A fashionable sector can still disappoint if expectations are too high.

Stock market cycles are not the same as economic cycles

Investors often talk about the economy and the stock market as if they move together. They are related, but they are not identical.

The economic cycle describes broad conditions such as expansion, slowdown, recession, and recovery. The stock market cycle describes investor behavior and asset prices. Because stocks reflect expectations about future profits, they often turn before the economic data clearly improves or deteriorates.

This is why recessions can be confusing for investors. By the time official data confirms a recession, the market may already have fallen significantly. The NBER business cycle dating committee identifies U.S. recessions after reviewing economic data, but investors must make decisions in real time.

The main lesson is that cycle analysis should be probabilistic. It helps you ask better questions, but it does not provide certainty.

Early recovery: cyclicals and small caps often lead

Early recoveries usually begin when news still looks bad. Earnings may be depressed, investors may be pessimistic, and economic headlines may still discuss recession risk. Yet stock prices can begin rising because the market starts to discount improvement.

In this phase, cyclical businesses often perform well. These are companies whose revenues and profits are sensitive to economic growth. Examples include industrial companies, banks, retailers, travel businesses, home improvement companies, and some technology hardware firms.

Consumer discretionary stocks can benefit when households feel more secure about income, employment, and wealth. People are more willing to book vacations, upgrade furniture, or improve their homes with items such as modern lighting for the home when confidence improves. That is why discretionary spending can be powerful during recoveries, although it can also fall sharply during downturns.

Small-cap stocks may also perform well early in a new bull market. Smaller companies are often more economically sensitive, more domestically focused, and more affected by credit conditions. When financing becomes easier and growth expectations improve, their earnings can rebound quickly.

The danger is quality. Early-cycle rallies can lift weak companies along with strong ones. Investors should avoid assuming that every beaten-down stock is a bargain. A low price is not the same as a low valuation, and a fallen stock is not automatically a good investment.

Mid-cycle expansion: broad equities and quality growth often shine

The mid-cycle phase is usually the most comfortable period for investors. Growth is positive, corporate profits are improving, and inflation is often under control. Market leadership can broaden beyond the most economically sensitive shares.

This is where broad equity exposure often works well. Index funds, diversified funds, and balanced stock portfolios can benefit because the market is not relying on one narrow group of winners.

Quality growth companies may also perform well. These are businesses with consistent revenue growth, strong margins, healthy balance sheets, and durable competitive advantages. Many technology, healthcare, and communication services companies can fit this description, although sector labels alone are not enough. A software company with high recurring revenue is different from a speculative company with no profits.

The mid-cycle phase can also create overconfidence. Investors may begin to believe that good conditions will last indefinitely. Valuations can expand, leverage can increase, and speculative behavior can return. That is when disciplined analysis matters. Greek Shares readers can review a structured approach in Stock Market Analysis Basics for Everyday Investors.

Late cycle: value, dividends, energy, and defensives may gain appeal

Late-cycle markets can feel strong on the surface. Stock indexes may still be near highs, unemployment may be low, and profits may remain healthy. Underneath, however, pressures may be building.

Inflation can rise. Central banks may keep interest rates high. Wage costs can squeeze margins. Credit can become tighter. Investors become more selective because future growth looks less certain.

In this environment, value stocks can sometimes outperform growth stocks. Value companies tend to have lower valuations, current earnings, and cash flows that investors can measure more easily. Dividend-paying companies may also attract attention, especially if they have a history of maintaining or increasing payouts.

Energy and materials may perform well when inflation is tied to commodity prices or supply constraints. However, these sectors can be volatile. Commodity-driven profits can rise quickly and fall just as fast.

Defensive sectors also become more attractive late in the cycle. Consumer staples, healthcare, and utilities sell products or services that people continue using even when the economy slows. Their earnings are not risk-free, but they may be less sensitive to recessions than highly cyclical industries.

Late cycle is also when high valuation becomes more dangerous. Long-duration growth stocks, meaning companies whose expected profits are far in the future, can be especially sensitive to higher interest rates. When discount rates rise, investors may pay less for distant future earnings.

Recession and bear markets: defense matters most

During recessions and bear markets, the question changes from how much can I make to how much can I avoid losing. Capital preservation becomes more important.

Cash and short-term government bills can be valuable because they provide liquidity and optionality. They allow investors to meet obligations, avoid forced selling, and buy assets later if valuations become attractive.

High-quality bonds may also perform well if interest rates fall during an economic slowdown. This is not guaranteed. The inflationary period after 2020 reminded investors that stocks and bonds can decline together when inflation and rates rise sharply. Still, high-quality bonds remain an important stabilizer for many portfolios.

Within equities, defensive sectors and quality companies often hold up better. Investors tend to favor businesses with stable demand, low debt, strong cash flow, and resilient margins. Companies that depend heavily on borrowing or aggressive growth assumptions can suffer when credit tightens.

Gold sometimes performs well during periods of stress, negative real interest rates, or currency concern. But gold does not produce earnings or dividends, so it should be understood as a potential diversifier, not a guaranteed recession winner.

The most important point is behavioral. Many investors sell during the worst part of a bear market and then wait for the economy to look safe again. The problem is that markets often recover before the news feels safe. Understanding why stocks fall can help investors separate temporary fear from permanent business damage.

The new bull market: the best returns often begin before confidence returns

The transition from bear market to bull market is one of the hardest periods to recognize in real time. Headlines may still be negative. Earnings may still be weak. Analysts may still be cutting forecasts.

Yet stocks can begin rising because expectations have become too pessimistic. If prices already reflect a severe outcome, even slightly better news can drive a powerful rally.

This is why all-in, all-out market timing is so difficult. If you wait for perfect confirmation, you may miss a significant part of the recovery. The early stage of a new bull market often rewards investors who were disciplined enough to rebalance, keep watchlists, and maintain exposure to quality assets.

For long-term investors, the best approach is usually not to guess the exact bottom. It is to have a written plan for when to buy, when to wait, and how much risk to take. Greek Shares covers that decision process in When to Buy Stocks and When to Wait.

Sectors matter, but investment styles matter too

Sector rotation gets a lot of attention, but performance is also shaped by investment styles, sometimes called factors. These include value, growth, quality, momentum, size, and low volatility.

| Investment style | When it may perform best | Main risk |

|---|---|---|

| Value | Late cycle, inflationary periods, recoveries from very low valuations | Cheap stocks can remain cheap if business quality is poor |

| Growth | Mid-cycle expansions, falling-rate environments, strong innovation cycles | High valuations can fall sharply when rates rise or expectations fade |

| Quality | Across cycles, especially slowdowns and uncertain markets | Quality can become overpriced when everyone seeks safety |

| Momentum | Strong trending markets and broad bull phases | Can reverse quickly during market turning points |

| Small caps | Early recoveries and improving credit conditions | More sensitive to recessions, financing costs, and liquidity stress |

| Low volatility | Recessions, defensive markets, risk-off periods | Can lag sharply during strong bull markets |

A factor is not a magic formula. It is a tendency that may be rewarded in some environments and punished in others. The key is to avoid building a portfolio that depends on only one outcome.

What indicators help identify the cycle?

No single indicator tells you exactly where the market cycle stands. A better approach is to combine several signals and watch whether they point in the same direction.

Useful indicators include:

- Interest rates and central bank policy: Falling rates can support valuations, while rising rates can pressure expensive assets.

- Inflation trends: Persistent inflation can favor real assets, energy, materials, and value stocks, while hurting long-duration growth stocks.

- Earnings revisions: If analysts are raising profit estimates broadly, the cycle may be improving. If estimates are falling, risk is rising.

- Credit spreads: Wider spreads suggest stress in credit markets and tighter financing conditions.

- Market breadth: A healthy bull market usually has many stocks participating, not only a few mega-cap leaders.

- Valuations: The same sector can be attractive or dangerous depending on price.

- Employment and consumer data: These help confirm economic strength or weakness, but they often lag the market.

Public data sources such as the Federal Reserve Bank of St. Louis FRED database can help investors track interest rates, credit spreads, inflation, and employment trends. For sector behavior by business cycle phase, Fidelity also maintains a useful overview of business cycle investing.

The practical portfolio lesson: do not make cycle calls too large

The best investors respect cycles without becoming slaves to them. They understand that a cycle tilt can help, but a wrong cycle call can be expensive.

A practical approach is to keep a diversified core and make only modest adjustments around it. For example, a long-term investor might hold broad equity exposure, bonds or cash for stability, and a smaller portion for sector or factor tilts. That way, the portfolio does not depend entirely on guessing the next phase correctly.

This is where asset allocation matters. Stocks may drive long-term growth, but bonds and cash can reduce the need to sell stocks during market stress. If you are comparing the roles of different asset classes, read Stocks vs Bonds: Which Fits Your Goals?.

Risk management matters more than being clever. Before trying to rotate sectors, investors should know their time horizon, income needs, risk tolerance, and maximum acceptable drawdown. A portfolio that looks optimal on paper is useless if you abandon it during the first major decline. Greek Shares expands on this in How to Manage Portfolio Risk Wisely.

Common mistakes when chasing cycle winners

One common mistake is identifying the cycle too late. By the time everyone agrees that a recovery is underway, many cyclical stocks may already have risen. By the time everyone fears recession, defensive stocks may already be expensive.

Another mistake is confusing sector strength with company strength. A poor business in a hot sector can still destroy capital. A good business in an unpopular sector can still create long-term value if bought at the right price.

Investors also tend to chase the last winner. After technology leads for years, they assume technology will always lead. After energy rallies, they assume energy will dominate forever. Markets punish this kind of linear thinking because expectations eventually become too optimistic.

Finally, many investors ignore taxes, fees, spreads, and emotional costs. Frequent rotation can look intelligent but produce poor after-tax results. A simple, disciplined portfolio often beats a complex strategy executed poorly.

So, what performs best in stock market cycles?

The best performer changes with the cycle, but the best process remains consistent.

In early recoveries, cyclicals, small caps, financials, consumer discretionary, and industrials often lead. In mid-cycle expansions, diversified equities and quality growth can do well. In late-cycle environments, value, dividends, energy, materials, and defensive sectors may become more attractive. In recessions, cash, high-quality bonds, defensive sectors, and strong balance sheets often matter most.

But the best long-term result usually comes from combining cycle awareness with discipline. That means diversifying, rebalancing, controlling risk, studying valuations, and avoiding emotional decisions.

A market cycle is not a script. It is a map. Use it to understand the terrain, not to pretend you know every turn in advance.

Frequently Asked Questions

What sector usually performs best during a recession? Defensive sectors such as consumer staples, healthcare, and utilities often hold up better because demand for their products and services is less sensitive to economic weakness. Cash and high-quality bonds may also perform well, depending on interest rates and inflation.

Do small-cap stocks perform best in stock market recoveries? Small caps often perform strongly early in recoveries because they are more sensitive to improving growth and credit conditions. However, they also carry higher risk, especially if balance sheets are weak or financing becomes expensive.

Is it better to rotate sectors or buy index funds? Many investors are better served by a diversified core, such as broad index funds, because sector rotation requires accurate timing and discipline. More experienced investors may use modest sector tilts, but they should avoid making the whole portfolio depend on one cycle forecast.

How do interest rates affect what performs best? Lower rates can support growth stocks and long-duration assets because future earnings become more valuable. Higher rates can pressure expensive growth stocks and favor value, dividends, financials, cash, or short-duration bonds, depending on the broader environment.

Can stock market cycles be timed perfectly? No. Market cycles can only be estimated. Economic data is often revised, official recession calls arrive late, and markets price expectations before the news is clear. A better goal is to manage risk and rebalance rather than predict exact tops and bottoms.

What is best for beginner investors during market cycles? Beginners should usually focus on diversification, regular investing, risk control, and understanding what they own. Trying to jump between sectors too early can lead to overtrading and emotional mistakes.

Keep learning with Greek Shares

Understanding stock market cycles is only one part of becoming a better investor. Continue building your foundation with Greek Shares tutorials, market guides, and risk management articles so your decisions are based on process, not panic or prediction.

{kind=link}