Most beginner investors do not fail because they lack access to advanced strategies. They fail because they try to make too many decisions too early, often with money they cannot afford to risk.

Useful investing is usually simpler than it looks. You need a clear goal, a realistic time horizon, a basic understanding of risk, and a repeatable process you can follow when markets are calm and when they are uncomfortable.

This guide focuses on investment tips beginners can actually use, not vague advice like buy low and sell high. Think of it as a practical starting framework you can adapt as your knowledge grows.

Before we begin, a quick note: this article is for education only. It is not personal financial advice. Your income, tax situation, location, debt, and goals all matter, so consider speaking with a qualified professional before making major decisions.

Start with a 5-minute investing readiness check

Investing works best when your basic financial foundation is stable. If you skip this step, even a good investment can become a problem because you may be forced to sell at the wrong time.

Ask yourself four questions before you invest your first dollar:

| Readiness question | Why it matters | Beginner-friendly target |

|---|---|---|

| Do I have money set aside for emergencies? | Prevents you from selling investments during a crisis | At least a small starter emergency fund, then build over time |

| Do I have high-interest debt? | Debt interest can erase investment gains | Prioritize expensive debt such as credit cards |

| When will I need this money? | Short timelines leave less room for market declines | Invest only money you can leave alone long enough |

| Can I contribute regularly? | Consistency matters more than perfect timing | A realistic monthly amount you can maintain |

If you are not ready yet, that is not failure. It is risk management. The strongest investors often start by improving their savings habits before buying anything.

Match every investment to a clear goal

A beginner mistake is asking, What should I buy? before asking, What is this money for?

Your goal determines your timeline, and your timeline determines how much risk you can reasonably take. Money needed next year should not be treated the same way as money intended for retirement decades from now.

| Goal type | Typical time horizon | What beginners should consider |

|---|---|---|

| Emergency savings | Immediate to 1 year | Cash or cash-like savings, not stocks |

| Home deposit or major purchase | 1 to 5 years | Lower-risk options may be more suitable |

| Long-term wealth building | 5 to 10+ years | Diversified funds may make sense |

| Retirement | Often 10+ years | A long-term portfolio with regular contributions |

If you are still deciding where your money belongs, Greek Shares has a helpful guide on where you can invest when you are just starting out based on different goals and time horizons.

The key idea is simple: do not invest all money the same way. Give each dollar a job.

Begin with an amount you can repeat

Many beginners delay investing because they think they need a large lump sum. In reality, a smaller amount invested consistently can help you build the habit without overwhelming your budget.

For example, if $25, $50, or $100 per month is realistic, that is a better starting point than investing $1,000 once and then stopping because your budget feels tight.

Regular investing can also reduce the pressure of choosing the perfect entry point. This is often called dollar-cost averaging, meaning you invest a set amount on a schedule. Sometimes you buy when prices are high, sometimes when prices are lower. It does not remove risk, but it can make the process easier to follow.

The best contribution amount is not the biggest number you can force this month. It is the amount you can continue during normal life.

Choose broad diversification before individual stock picking

Buying individual stocks can be exciting, but it is usually not the simplest first step. A single company can face unexpected problems, including poor earnings, management mistakes, regulation, competition, or industry disruption.

Diversified funds, such as broad-market index funds or ETFs, spread your money across many companies. That does not guarantee profit, but it reduces the risk of one business damaging your entire plan.

According to the U.S. Securities and Exchange Commission investor education site, diversification helps reduce the risk that poor performance from one investment will heavily damage your portfolio. You can explore its beginner-friendly explanation at Investor.gov.

For many beginners, a simple diversified core is easier to manage than a basket of random stocks found through social media, news headlines, or friends.

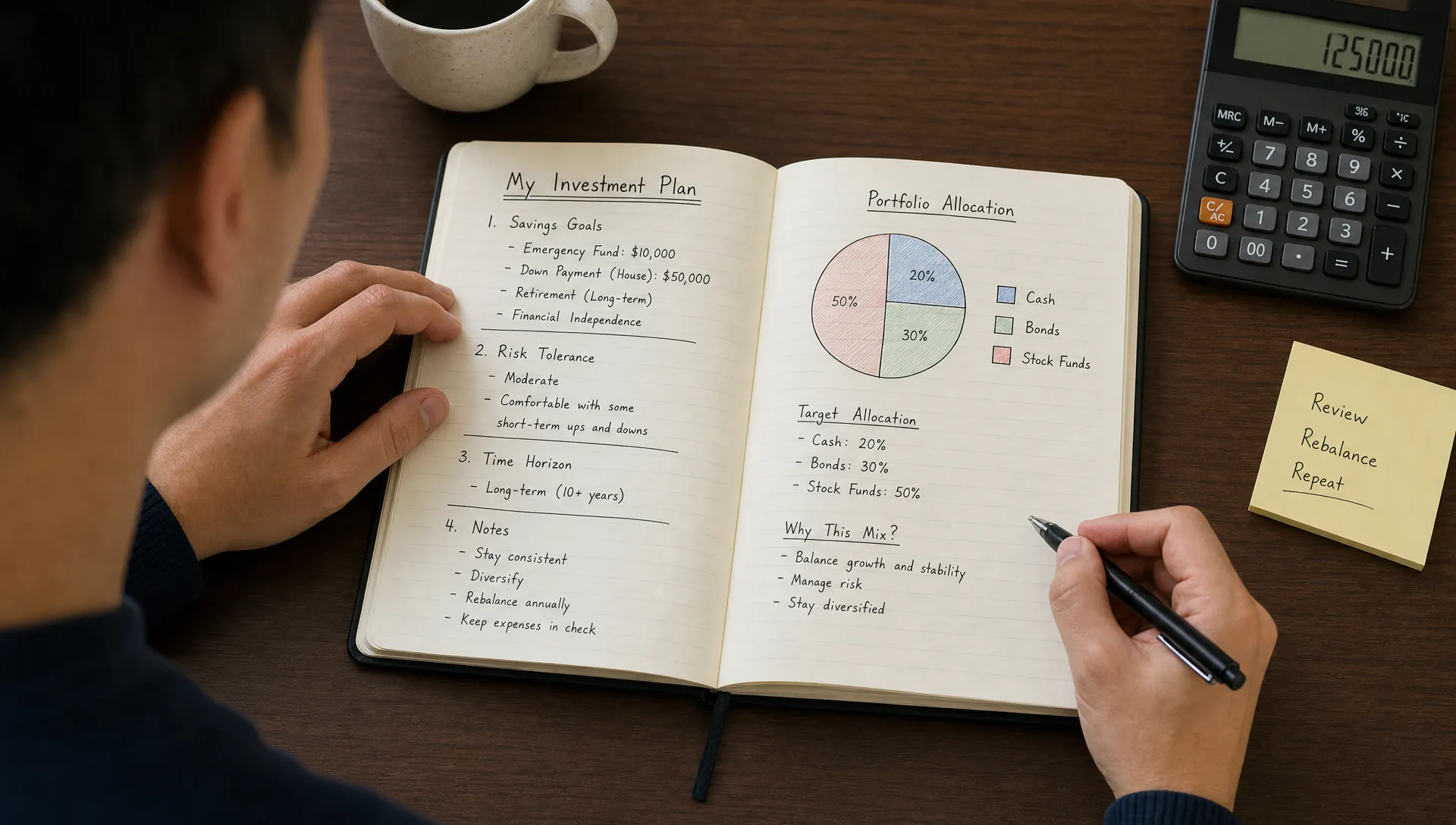

Build a simple first portfolio, not a perfect one

A first portfolio should be understandable. If you cannot explain what you own and why you own it, the portfolio is probably too complex.

A beginner portfolio often includes a mix of growth assets, such as stock funds, and stability assets, such as bonds or cash, depending on time horizon and risk tolerance. The right mix is personal, but the structure should be easy to review.

| Portfolio style | General idea | Who might consider learning about it |

|---|---|---|

| Conservative | More focus on stability and lower volatility | Investors with shorter timelines or low risk tolerance |

| Balanced | Mix of growth and stability | Investors who want moderate risk and diversification |

| Growth-oriented | More exposure to stocks and long-term growth | Investors with long timelines and higher risk tolerance |

A simple portfolio is not boring. It is easier to maintain, easier to rebalance, and easier to understand during market declines. If you want a deeper walkthrough, start with this beginner portfolio building guide, which explains goals, risk tolerance, and portfolio basics in more detail.

Understand what you are buying before you buy it

One of the most practical investing tips for beginners is also one of the most ignored: pause before every purchase and explain the investment in plain English.

For an ETF or index fund, you should understand:

- What market or index it tracks

- What types of companies or assets it holds

- How much it charges in annual fees

- Whether it fits your goal and time horizon

- What could cause it to lose value

For an individual stock, you should understand the business, not just the ticker symbol. Ask how the company makes money, whether it is profitable, how much debt it carries, what competitors threaten it, and whether the current price already reflects high expectations.

This habit also applies outside the stock market. Sometimes the best investment is increasing your earning power. That could mean learning a skill, improving your sales process, or, for a founder, exploring a specialist such as DirectB2BLeads for B2B customer acquisition if qualified sales calls are a real business bottleneck. The principle is the same: understand the expected return, the risk, and why the spending fits your goal.

Set buying and selling rules before emotions take over

Markets test emotions. When prices rise quickly, beginners may feel they are missing out. When prices fall, they may feel they must sell immediately. Both reactions can lead to poor decisions.

Create simple rules before you invest. They do not need to be complicated, but they should be written down.

Useful beginner rules include:

- I will not invest money I need for bills, rent, or short-term goals.

- I will not buy an investment just because it is trending online.

- I will wait at least 24 hours before making a large new purchase.

- I will review my portfolio on a schedule, not every time the market moves.

- I will sell because my plan changed, not because I feel panic.

Rules protect you from making permanent decisions based on temporary emotions.

Pay attention to fees because small numbers compound

Fees may look harmless, especially when they are shown as small percentages. But over many years, fees can quietly reduce your returns.

For example, a fund charging 0.10% annually costs much less than one charging 1.00% annually. The difference may not feel dramatic in year one, but over decades it can become meaningful because the money paid in fees no longer compounds for you.

This does not mean the cheapest option is always best. It means beginners should know what they are paying and why. If an investment, app, advisor, or fund charges a fee, ask what value you receive in return.

Also remember taxes. Selling investments can create taxable events depending on your country, account type, and holding period. Tax rules vary widely, so avoid assuming that investment returns are the same as after-tax returns.

Automate contributions, but do not automate ignorance

Automation is powerful. A recurring investment can remove the need to remember each month and reduce the temptation to time the market.

However, automation should not mean ignoring your portfolio completely. A good rhythm for beginners is to automate contributions and schedule occasional reviews.

A simple review schedule might look like this:

| Review frequency | What to check |

|---|---|

| Monthly | Confirm contributions were made and your budget still works |

| Quarterly | Review performance, fees, and whether your allocation drifted |

| Annually | Revisit goals, risk tolerance, income, taxes, and major life changes |

Do not confuse checking with reacting. Looking at your account every day can make normal market movement feel urgent. Long-term investing usually rewards patience more than constant activity.

Learn the common mistakes before they cost you money

Beginners often think investing mistakes come from choosing the wrong stock. Sometimes they do, but many mistakes are behavioral.

Common early mistakes include investing without an emergency fund, chasing past performance, copying influencers, ignoring fees, concentrating too much money in one company, and selling during panic.

The good news is that most of these mistakes are avoidable. If you want a practical checklist, read Greek Shares' guide to stock market investing mistakes to avoid early on before placing your first trades.

Learning what not to do can save you years of frustration.

A beginner action plan for the next 30 days

If you feel overwhelmed, use this simple 30-day plan. The goal is not to become an expert in one month. The goal is to move from confusion to a basic, repeatable process.

- Write down your top three financial goals and when you need the money.

- Separate short-term savings from long-term investing money.

- Check whether you have high-interest debt that should be prioritized.

- Choose a realistic monthly investing amount that does not stress your budget.

- Learn the basics of diversified funds, fees, and risk before buying.

- Create written rules for buying, selling, and reviewing your portfolio.

- Make your first investment small enough that you can stay calm and learn.

This approach may feel slow, but slow is often safer for beginners. You are not just buying investments. You are building judgment.

Frequently Asked Questions

What is the best investment for beginners? There is no single best investment for every beginner. Many new investors start by learning about diversified index funds or ETFs because they spread risk across many holdings, but your best choice depends on your goals, timeline, risk tolerance, and financial foundation.

How much money should a beginner invest? Start with an amount you can repeat without hurting your budget. Consistency matters more than size. If a small monthly amount helps you build the habit and stay invested, it can be a smart starting point.

Should beginners buy individual stocks? Beginners can learn about individual stocks, but it is usually safer to build a diversified core first. Individual stocks require research, patience, and the ability to handle company-specific risk.

Is it risky to invest when the market is high? Investing always involves risk, and markets can fall after you invest. A long time horizon, diversification, and regular contributions can help reduce the pressure of trying to pick the perfect entry point.

How often should beginners check their investments? Checking too often can encourage emotional decisions. Many beginners benefit from monthly budget checks, quarterly portfolio reviews, and a deeper annual review of goals and risk tolerance.

Keep your investing plan simple enough to follow

The best beginner investment plan is not the one that sounds impressive. It is the one you understand, can afford, and can follow through market ups and downs.

Start with your financial foundation. Match investments to goals. Favor diversification before speculation. Keep fees low where possible. Write down your rules. Review your plan on a schedule.

If you want to keep building your knowledge step by step, explore more beginner investing guides on Greek Shares. The more clearly you understand your own plan, the less likely you are to be pushed around by headlines, hype, and short-term market noise.

{kind=link}