Investing does not have to start with complex charts, hot stock tips, or daily market predictions. If you want to learn how to invest in stocks, the most useful first step is building a simple plan you can actually follow when markets are calm, noisy, rising, or falling.

A stock is a share of ownership in a business. When you invest in stocks, you are not just buying a ticker symbol. You are putting money into companies, industries, and economies with the expectation that, over time, business growth can reward patient owners. That reward is never guaranteed, and prices can move sharply in the short term. A plan helps you stay rational anyway.

This guide is educational, not personal financial advice. Use it to understand the moving parts, then adapt the ideas to your goals, timeline, income, risk tolerance, and local tax rules.

Start With the Reason You Are Investing

Before opening a brokerage account or choosing a stock, define what the money is for. A vague goal like “make more money” is not enough. It gives you no guidance when the market drops, a stock doubles, or a social media influencer says the next big opportunity is here.

A useful investing goal answers three questions: what are you investing for, when do you expect to use the money, and how much risk can you emotionally and financially handle?

For example, investing for retirement in 25 years is very different from saving for a home deposit in two years. Stocks can be powerful long-term wealth-building tools, but they are not ideal for money you may need soon. Short timelines leave less room to recover from market declines.

| Goal type | Typical time horizon | Stock exposure may be appropriate? | Main priority |

|---|---|---|---|

| Emergency savings | Immediate to 12 months | Usually no | Safety and liquidity |

| Home deposit or tuition soon | 1 to 3 years | Usually limited or no | Capital preservation |

| Major goal later | 5 to 10 years | Possibly, depending on risk tolerance | Balanced growth and stability |

| Retirement or long-term wealth | 10+ years | Often yes | Long-term growth |

If you are still building your financial foundation, it may help to review how to approach stocks only after you have the basics in place. Greek Shares has a helpful guide on how to invest in stocks the smart way as a beginner that covers budgeting, debt, and preparation before buying shares.

Build a Safety Margin Before You Buy

A simple stock investing plan begins outside the stock market. The goal is to avoid being forced to sell investments at the wrong time because life happened.

Start with an emergency fund that can cover essential expenses. The exact amount depends on your job stability, household responsibilities, and monthly costs, but the purpose is the same: protect your investing plan from sudden bills, income interruptions, or urgent repairs.

Next, look at high-interest debt. If you are paying very high rates on credit cards or similar debt, paying that down can be a more reliable improvement to your financial position than taking market risk. Investing while expensive debt compounds against you can feel like running forward while being pulled backward.

Planning matters in any field where timing and decisions can affect long-term outcomes. For example, digital orthodontics with 3D planning maps the treatment path before movement begins. Investors can borrow the same mindset: define the structure first, then act with discipline instead of improvising under pressure.

Choose the Right Investment Account and Broker

Once your goal and foundation are clear, choose where your investments will live. Depending on your country, you may have access to retirement accounts, tax-advantaged accounts, or standard taxable brokerage accounts. Tax rules vary widely, so it is worth checking local regulations or speaking with a qualified professional if you are unsure.

When comparing brokers, beginners often focus only on app design. A clean interface is nice, but the more important factors are reliability, regulation, costs, available investments, educational resources, and whether the platform encourages thoughtful investing instead of constant trading.

Look for a broker that makes it easy to buy diversified investments, understand fees, and place orders clearly. Low commissions matter, but hidden costs, currency conversion fees, spreads, fund expense ratios, and inactivity fees can also affect returns over time.

A beginner-friendly broker should help you do boring things well. Boring is not a weakness in investing. In many cases, the boring plan is the one that survives.

Decide What You Will Buy Before You Fund the Account

Many beginners transfer money first, then ask, “What should I buy today?” That order creates pressure. It is better to decide your investment approach before cash is waiting in the account.

Most long-term beginners can think in terms of a core and, only if appropriate, a smaller satellite portion. The core is the main engine of the portfolio, usually built around broad diversification. The satellite portion is optional and might include individual stocks, sector funds, or other investments you understand well.

| Portfolio part | Purpose | Common beginner approach | Risk level |

|---|---|---|---|

| Core | Long-term growth through diversification | Broad-market index funds or ETFs | Market risk, but spread across many holdings |

| Satellite | Learning, personal conviction, or targeted exposure | A few researched individual stocks | Higher, because concentration increases risk |

| Cash reserve | Stability and flexibility | Savings or cash-like instruments | Lower, but inflation can reduce purchasing power |

Diversified funds can reduce company-specific risk because your money is spread across many businesses. If one company struggles, it does not necessarily determine the outcome of your whole portfolio. This is one reason many beginners start with index funds or ETFs rather than trying to pick winning stocks from day one.

Individual stocks are not automatically bad. They simply require more understanding. You should be able to explain what the company does, how it makes money, what could go wrong, how much debt it has, whether profits are growing, and whether the price seems reasonable compared with the business quality. If you want a framework for that research, Greek Shares explains the foundations in its guide to stock market analysis basics.

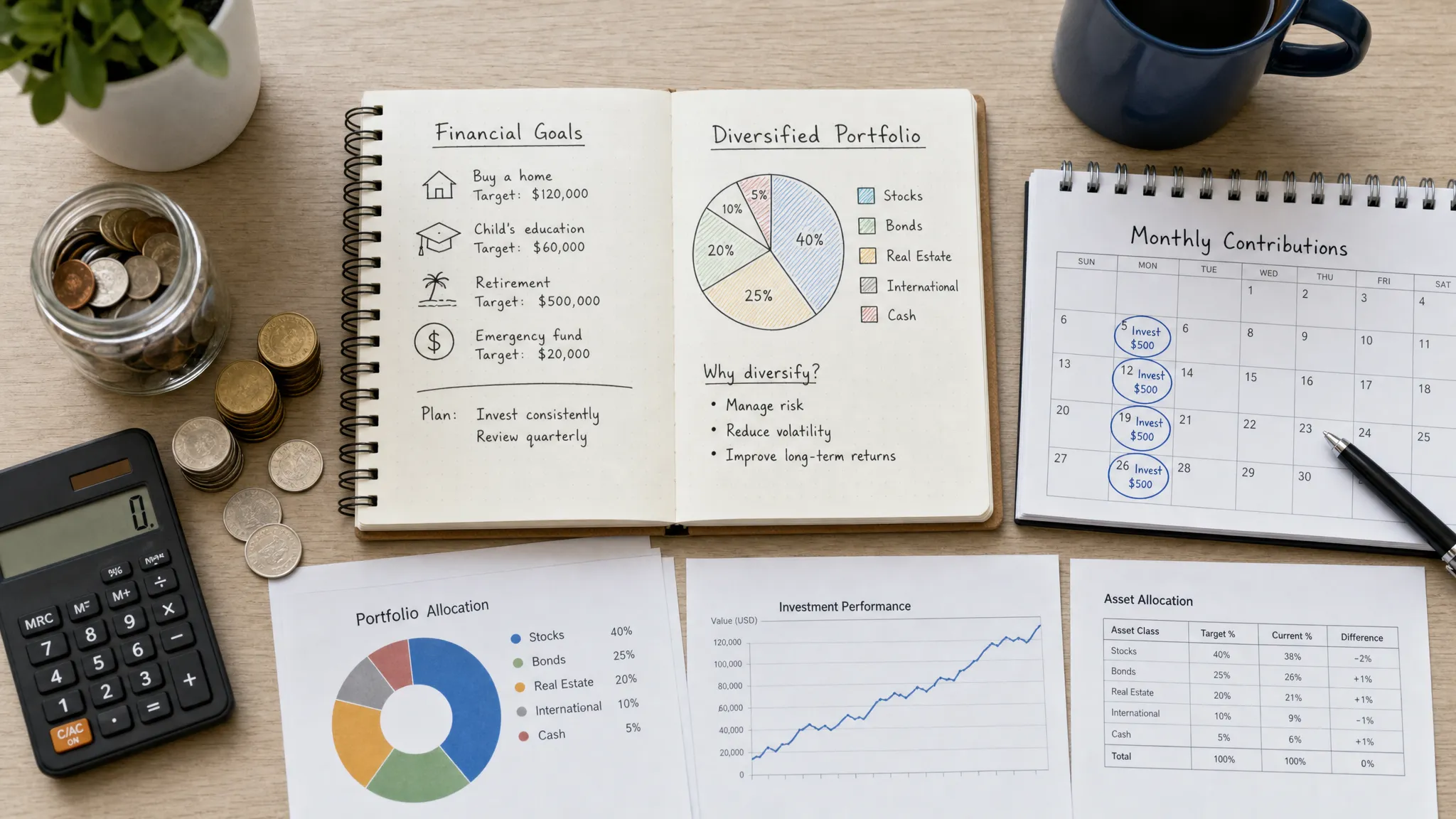

Use a Simple Allocation Rule

Asset allocation means deciding how much of your portfolio goes into stocks, bonds, cash, or other assets. It is one of the most important decisions you make because it affects both potential return and emotional difficulty.

A portfolio with more stocks may offer higher long-term growth potential, but it can also fall more sharply during market downturns. A portfolio with more cash or bonds may feel steadier, but it may grow more slowly. There is no perfect allocation for everyone.

Instead of searching for a magic formula, choose an allocation that matches your time horizon and your ability to stay invested. If a 30% market drop would cause you to sell everything, your allocation is probably too aggressive, even if it looks optimal in a spreadsheet.

A simple beginner test is to ask: “If my portfolio fell by 20% this year, would I still follow the plan?” If the honest answer is no, reduce risk before the market forces the lesson.

Set a Buying Schedule

One of the hardest parts of investing is deciding when to buy. A simple plan removes much of that stress by using a schedule.

Many beginners use regular contributions, such as monthly investing after income arrives. This approach is often called dollar-cost averaging. It does not guarantee profits or protect against losses, but it can reduce the pressure of trying to pick the perfect day. You buy more shares when prices are lower and fewer shares when prices are higher.

The most important part is consistency. A small amount invested regularly can build discipline, especially when paired with automatic transfers. Starting small is acceptable. In fact, it can be wise. Your first goal is not to prove you are brilliant. Your first goal is to learn the mechanics without risking money you cannot afford to lose.

Your buying schedule should include these basic rules:

- How much you plan to invest each month or quarter.

- Which investments receive the contribution.

- What conditions would make you pause, such as job loss or emergency fund depletion.

- How often you will review your plan.

Notice what is missing: predictions. A simple investing plan does not require you to know what the market will do next week.

Learn the Basic Order Types Before Clicking Buy

Buying stocks or ETFs is mechanically simple, but small misunderstandings can cause frustration. Two common order types are market orders and limit orders.

A market order buys or sells at the best available current price. It is usually fast, but the exact execution price can differ from the last price you saw, especially in volatile or thinly traded investments.

A limit order sets the maximum price you are willing to pay when buying, or the minimum price you are willing to accept when selling. It gives more price control, but the order may not execute if the market does not reach your limit.

For highly liquid ETFs or large stocks during normal market hours, the difference may be small. For less liquid securities, volatile markets, or trading outside regular hours, order type matters more.

If you want a practical walkthrough of the mechanics, including brokerage accounts, funding, and placing orders, Greek Shares has a dedicated article on how to buy stocks the right way.

Protect Yourself With Risk Rules

Risk management is not about avoiding all losses. Losses are part of investing. Risk management is about preventing one mistake, one stock, or one emotional decision from damaging your long-term plan.

A few rules can make a major difference. Avoid putting all your money into one company, no matter how strong the story sounds. Be careful with leverage, margin, and options if you are still learning. Do not invest money needed for bills, rent, taxes, or near-term commitments. Keep records of why you bought each investment so you can review decisions calmly later.

Position sizing is especially important for individual stocks. If one stock is 2% of your portfolio, a bad outcome hurts but may be manageable. If one stock is 60% of your portfolio, the same bad outcome can change your financial life.

Also remember that risk is not only price volatility. A stock can be risky because the business is weakening, the valuation is too high, the industry is changing, the balance sheet is fragile, or the investor does not understand what they own.

Review Your Portfolio Without Overreacting

A simple plan should include a review rhythm. Too little attention can lead to neglect. Too much attention can lead to emotional trading. For many long-term beginners, a quarterly or semiannual review is enough, with a deeper annual review.

During a review, ask whether your goals, income, time horizon, or risk tolerance have changed. Check whether your portfolio still matches your target allocation. If one part has grown too large, you may need to rebalance by directing new contributions elsewhere or, in some cases, selling a portion.

You do not need to react to every headline. Markets will always have reasons to worry: interest rates, inflation, elections, earnings, wars, recessions, new technologies, and investor sentiment. A plan helps you separate important personal changes from background noise.

Your review should focus on questions you can control:

- Did I contribute according to my schedule?

- Is my emergency fund still adequate?

- Is my portfolio still diversified?

- Did I buy anything I do not understand?

- Am I making decisions based on a plan or emotion?

These questions are not exciting, but they are powerful.

Avoid the Beginner Mistakes That Break Good Plans

Many investing mistakes come from impatience. Beginners often want fast confirmation that they made the right choice. When a stock rises, they feel smart. When it falls, they feel foolish. Neither reaction is reliable.

One common mistake is chasing recent winners. A stock or sector that has already risen sharply may continue rising, but it may also be priced for unrealistic expectations. Buying only because something went up is speculation, not analysis.

Another mistake is panic selling during normal market declines. Long-term investors should expect declines. The stock market does not move upward in a straight line. If every drop feels like an emergency, your allocation may be too risky or your plan may not be clear enough.

A third mistake is confusing activity with progress. Checking prices ten times a day, switching strategies weekly, and reacting to every opinion online can make investing feel productive while actually increasing mistakes. Good investing often feels slow because compounding needs time.

Finally, avoid investing in anything you cannot explain. Complexity can hide risk. If you do not understand how an investment makes money, what could cause losses, and what fees apply, pause and learn before committing capital.

A Simple Stock Investing Plan You Can Follow

Here is a straightforward plan to bring everything together.

| Step | Decision | Simple action |

|---|---|---|

| 1 | Goal | Define what the money is for and when you may need it |

| 2 | Foundation | Build emergency savings and manage high-interest debt |

| 3 | Account | Choose a regulated broker and suitable account type |

| 4 | Investments | Start with a diversified core before considering individual stocks |

| 5 | Schedule | Invest a fixed amount regularly, if your finances allow |

| 6 | Risk | Limit concentration and avoid money needed soon |

| 7 | Review | Check progress on a set schedule, not every market move |

This plan is simple, but simple does not mean careless. It gives every dollar a role, every purchase a reason, and every review a structure. That is exactly what many beginners need.

If you want to learn how to invest in stocks, do not start by asking which stock will rise next. Start by asking what kind of investor you are trying to become. The answer should be patient, informed, diversified, and consistent.

Frequently Asked Questions

How much money do I need to start investing in stocks? You do not need a large amount to start learning. Many brokers allow small purchases or fractional shares, but you should only invest after covering essential expenses, building emergency savings, and understanding the risks.

Are individual stocks better than index funds? Not necessarily. Individual stocks can offer higher potential returns, but they also create more company-specific risk. Broad index funds or ETFs are often simpler for beginners because they provide diversification in one investment.

What is the safest way to invest in stocks? No stock investment is completely safe. A more cautious approach is to diversify, invest for the long term, avoid leverage, keep cash for short-term needs, and use an allocation you can hold through downturns.

Should I wait for the market to fall before investing? Waiting can feel logical, but market timing is difficult. A regular buying schedule can help reduce the pressure of predicting short-term movements while building long-term discipline.

How often should I check my investments? Long-term beginners usually do not need to check daily. A quarterly, semiannual, or annual review may be enough, unless your personal finances or goals change.

Keep Learning Before You Risk More

The best investing plan is one you understand well enough to follow when emotions rise. Start small, keep your process simple, and treat every decision as part of a long-term education.

Greek Shares offers beginner-friendly investing articles, stock market guides, financial terms, and practical tutorials to help you build confidence step by step. Use those resources to keep improving your plan before adding more risk.

{kind=link}